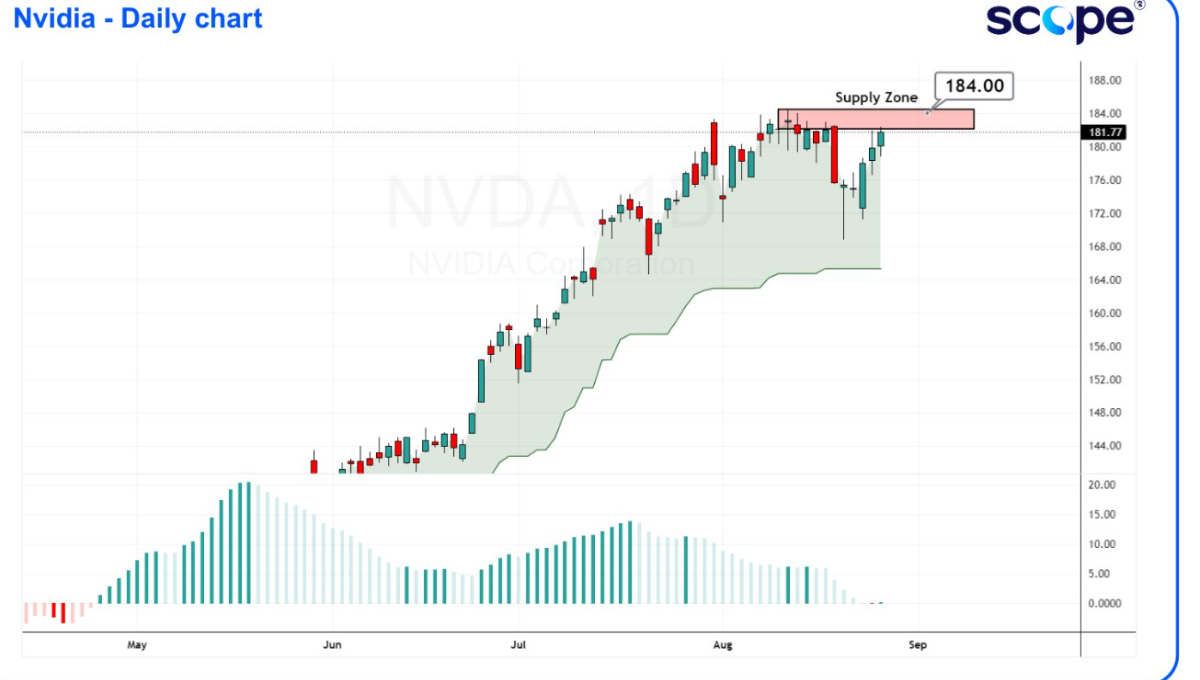

Nvidia Stock Price is on center stage again as investors brace for Q2 FY26 results after the closing bell today. As of this writing, NVDA is trading around $182 intraday, up modestly on the session, with the tape unusually calm for such a consequential print. The quiet won’t last: options markets are braced for a large swing once numbers hit and guidance rolls out.

Why today matters

Nvidia has become the gravitational center of the AI trade and, by extension, of global equities. The company crossed the $4 trillion market-cap milestone earlier this summer—an achievement that crowned it the world’s most valuable public company and set a new bar for tech bellwethers. Today’s report will test whether the growth arc behind that valuation can keep bending upward.

Earnings timing and where to listen

Management will report Q2 FY26 (quarter ended July 27, 2025) after market close, with a webcast slated for 2:00 p.m. PT. If you want the primary source, bookmark Nvidia’s investor relations page for the live audio and slides (official webcast link).

What Wall Street expects

Consensus heading into the print looks like this: revenue around $46.0 billion (up ~53% year over year) and EPS near $1.01 (up ~49%). While those are breathtaking comps by any normal standard, they also represent a deceleration versus the extraordinary triple-digit growth of prior periods, so investors will scrutinize forward guidance even more than the headline beat/miss.

The setup: implied move and sentiment

Derivatives markets are pricing a sizable reaction. Multiple outlets note traders are braced for an after-hours move that could translate into an eye-watering $260 billion swing in market value, depending on how revenue, margins, and supply commentary land. In the hours before the report, futures and the broader tech complex were relatively muted, underscoring just how dominant Nvidia-specific risk is in today’s tape.

Valuation in context

On a near-term basis, NVDA has traded ~33–34× next-12-month earnings—rich versus the S&P 500 but lower than prior peaks for a company still growing revenue at a breakneck pace. That multiple will expand or compress on tonight’s numbers, the demand outlook for Blackwell systems, and any updates on China-related headwinds.

What could move the nvidia stock price tonight

- Blackwell & GB200 ramp clarity. Investors want detail on the delivery cadence of Blackwell-generation platforms and the total cost of ownership improvements versus Hopper. The faster hyperscalers and AI-native clouds can stand up GB200/NVL systems, the firmer the 2026 demand line looks. Even small phrasings about “supply catching up” can swing multi-billions in expected capex.

- Networking attach & AI factory narrative. Nvidia’s platform story now includes high-performance Ethernet for AI fabrics. Last week the company introduced Spectrum-XGS Ethernet—“scale-across” tech meant to unify distributed data centers into giga-scale AI super-factories. Any color on pipeline, pricing, and margin mix here will matter for out-year models.

- Enterprise AI beyond hyperscale. The company highlighted adoption of RTX PRO Servers—Blackwell-based infrastructure that lets enterprises upgrade into AI without ripping out entire data centers. Watch for customer logos and vertical breakouts (design, media, digital twins).

- China exposure and compliance. Analysts will press for an update on U.S. export rules and any workarounds. Recent coverage flagged potential revenue impacts in the multi-billion range from tightened controls; how Nvidia navigates those constraints (product variants, geographic mix) will feed scenario analysis for FY26/27.

- Gross margin trajectory. Street models have baked in elite margins for AI silicon and systems; commentary about mix shift (more networking and systems vs. standalone GPUs) could nudge the margin arc either way.

Macro stakes: when one ticker sways the whole market

It’s not an exaggeration to say NVDA has been the market’s fulcrum. In recent sessions, indices have chopped sideways as traders wait for this print to either validate the AI capex wave—or hint at digestion. Wire services this morning framed it explicitly: Wall Street is in a countdown to Nvidia’s results, with tech valuations and the broader rally’s durability on the line.

How we got here: the $4T club

On July 9, 2025, Nvidia became the first public company to cross a $4 trillion market cap—an AI-era milestone later joined by Microsoft. Since then, leadership has see-sawed, but Nvidia’s lead over runner-up megacaps recently widened to roughly $700 billion, underscoring how uniquely levered the company is to the current build-out of AI compute.

Risks that every NVDA holder should keep in view

- Export policy & geopolitics: U.S.–China rules can shift quickly, changing product roadmaps and addressable markets. Recent reporting highlighted sizeable revenue headwinds tied to tightened export controls.

- Competition: Hyperscalers are advancing their own accelerators; AMD and Intel are iterating rapidly. The question isn’t whether Nvidia remains best-in-class, but whether it stays far enough ahead to defend pricing and margins.

- Supply chain & capacity: Even with more substrate, packaging, and foundry capacity online, appetite for AI compute has outpaced supply. Any signal that demand > supply is easing could compress the “scarcity premium.”

- AI returns debate: Studies and CEO commentary questioning near-term productivity gains can dampen enthusiasm if enterprises slow pilots or stretch deployments.

Scenarios to watch after the bell

Goldilocks beat & raise: Clean top- and bottom-line beats, guide above consensus, confident language on Blackwell shipments and networking attach → multiple can hold or expand, and the market refocuses on 2026 earnings power.

Beat but cautious guide: Strong Q2 but tempered guide on supply timing or China mix → profit-taking possible given the year-to-date run, even if the long-term story remains intact.

Mixed print, mixed signals: If revenue/margins land fine but commentary hints at digestion—or enterprise AI is slower than hoped—options pricing implies the stock could swing sharply as multiples recalibrate.

For investors tracking the nvidia stock price day to day

NVDA’s near-term rhythm is event-driven. Into and out of earnings, intraday moves often trace headlines: hyperscaler capex updates, data-center build-outs, or product milestones like Spectrum-XGS Ethernet and RTX PRO Servers. But price discovery ultimately comes back to three questions: (1) how fast the AI factory build continues, (2) how much of that spend Nvidia captures across compute + networking + software, and (3) how durable those margins look as competitors scale.

Bottom line

The nvidia stock price is calm on the surface, but a lot of energy is building underneath. Expectations call for ~53% revenue growth and ~49% EPS growth, with the Street laser-focused on the Blackwell ramp, networking attach, and China exposure. Options are pricing a very large move.

Whether tonight’s commentary extends Nvidia’s $4T-era lead—or invites a breather—will set the tone not just for semis, but for the entire AI trade.

Fast facts (updated intraday)

- Price (intraday): about $182 (see live chart above).

- Earnings call: Today at 2:00 p.m. PT (Q2 FY26).

- Market cap milestone: First public company to hit $4T (July 9, 2025); Microsoft later joined.

- Implied move: Options point to potential ~$260B market-cap swing.

- Recent product news: Spectrum-XGS Ethernet; RTX PRO Servers adoption.